Hadrien de Cournon and Henri Delahaye are the co-founders of RAISE Summit, taking place July 8–9, 2026, at the Carrousel du Louvre in Paris.

Three years is enough time to watch a technology cycle change shape. In 2024, when we hosted the first RAISE Summit in Paris, enterprise conversations about AI were about discovery: what is this technology, and what could it mean for us? In 2025, the theme was experimentation. Pilots multiplied, coding assistants broke through as the first use case with quantifiable returns, and CFOs started asking about token budgets.

In 2026, the question has changed again. Boards are no longer asking whether AI works. They are asking why it isn't yet showing up in the P&L. This is the execution era, and it exposes a gap the industry has been reluctant to name.

The gap between AI-native growth and enterprise pace

AI-native companies are growing at rates the software industry has rarely seen. Some are already becoming buyers of the next wave of AI-native startups. But inside our own bubble, it is easy to miss a harder truth: most large enterprises have not changed their pace at anything like the same rate.

Adoption inside a Fortune 1000 company happens from two directions at once. It comes from the top, where CIOs, CTOs and chief AI officers set architecture, procurement and governance. And it comes from the bottom, where developers decide which tools and stacks actually get used, and pull them up through engineering leadership. Companies selling AI need to work both channels. Most only work one.

That diagnosis shaped the biggest change to RAISE in 2026. The CxO Summit, launching July 8 at the Carrousel du Louvre, is an invitation-only forum that puts technology leaders from Fortune 1000 and CAC 40 companies (Airbus, BNP Paribas, Sanofi, Bank of America, and Mercedes-Benz among them) in direct, Chatham House-rule conversation with the CEOs of the AI companies they now buy from. QuantumBlack, AI by McKinsey, joins as a knowledge partner. The agenda is deliberately unglamorous: agentic systems in production, workforce transformation, and how to measure ROI in terms a board will accept.

Sovereignty stopped being an excuse

The second shift of 2026 is geopolitical. Two years ago, "sovereign AI" was widely read as a defensive argument, the pitch you made when you couldn't compete on capability. That framing is dead. Today, sovereignty sits on the roadmaps of telecoms operators, banks, and financial institutions across Europe as a hard requirement.

What we hear from partners and sponsors is that there is no single sovereign playbook. At the infrastructure layer, decisions go country by country: build an AI gigafactory in France, and you will likely partner with a French neocloud or data center operator. At the model layer, consolidation has started. Aleph Alpha, long Germany's leading LLM developer, merged with Canada's Cohere to pursue exactly this sovereign go-to-market position. At the application layer, partnerships such as Liquid AI's work with Mercedes-Benz show how edge and on-premise deployment are re-entering enterprise architecture discussions.

The commercial logic has inverted. Being sovereign no longer signals that you are a weaker alternative. If your product matches your competitors on capability and you are sovereign on top of it, the choice becomes straightforward for a European buyer. That is a tailwind, and French and European AI-native companies like Mistral, ElevenLabs, Lovable, and H Company are riding it on merit because they deliver.

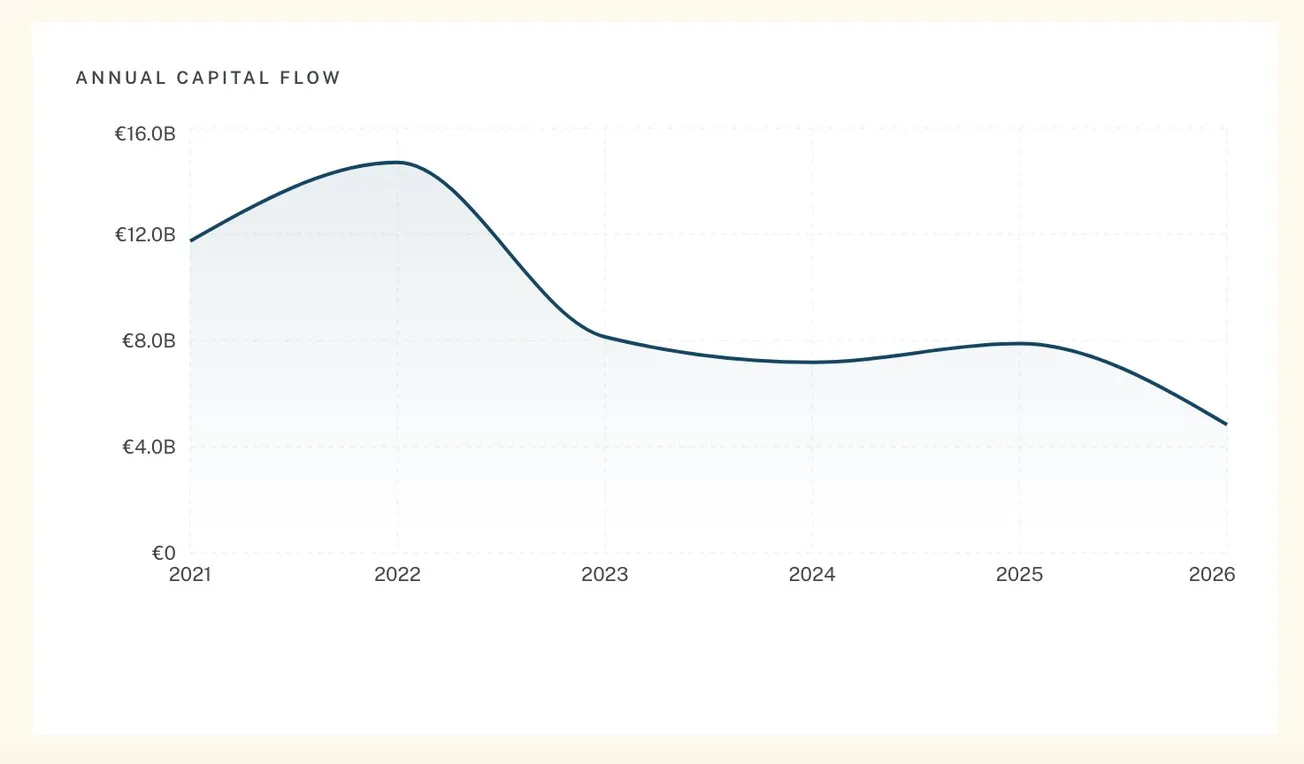

The capital data supports this reading. The French Tech Journal's H1 2026 funding report recorded €4.83B raised by French startups in the first half of the year, with a small number of very large AI deals driving most of the growth. Concentrated, conviction-driven capital is exactly what an execution era looks like.

Physical AI gets its own stage

One category has moved fast enough to demand a dedicated forum. Humanoid robots are leaving research labs for factory floors, industrial autonomy is scaling across logistics and manufacturing, and the foundation models that act as the "robot brain" are evolving on their own trajectory.

On July 7 at Station F, we launch MACHINA Summit, the first major European event dedicated entirely to Physical AI. The program covers the full stack across four tracks: humanoids, industrial deployment, simulation and training, and AI-robotics integration. Speakers include Jim Fan (NVIDIA), Carolina Parada (Google DeepMind), Marc Raibert (RAI Institute / Boston Dynamics), and Jeff Cardenas (Apptronik). Europe has real industrial depth in robotics. It should host the conversation about where the field goes next.

Why this happens in Paris

RAISE Summit returns to the Carrousel du Louvre on July 8–9 with more than 9,000 attendees, over 350 speakers, 80% of participants at C-level, and roughly 30% traveling from the United States. Around it, RAISE Week (July 4–9) spans a hybrid hackathon with 500 developers on site and 5,000 online, a startup competition with over €10M in prizes, and more than 50 partner events across the city, including a frontier-model gathering that brings Chinese, European and American lab researchers into the same room, which still happens too rarely.

Paris earns this role. France is now home to one of Europe's strongest concentrations of AI companies, labs, and capital, and its position allows a summit here to serve as neutral ground: a bridge between American capital and platforms, European enterprises and regulators, and growing delegations from the Middle East and Asia. Everyone does business together. They need a place designed for it.

The takeaway for founders and investors

Our metric for the event is unchanged and unfashionable: return on investment, measured in the meetings that matter. In 2025, RAISE facilitated more than 1,500 one-to-one meetings among 7,000 delegates, including 822 CEOs and investors managing over $600B in assets.

For founders, the execution era means distribution is now the hard problem. Selling to enterprises requires winning developers and technology leadership simultaneously, and sovereignty requirements will increasingly shape which vendors make the shortlist. For investors, the signal has moved from model benchmarks to deployment evidence: which companies are actually inside enterprise workflows, and at what margin.

The discovery phase rewarded vision. The experimentation phase rewarded speed. The execution era rewards proof. That is the standard we are building RAISE around, and the standard we would suggest applying to every AI claim you hear this year, including ours.

{kind=link}