There's a version of the Q2 2026 French tech funding story that offers a comforting narrative.

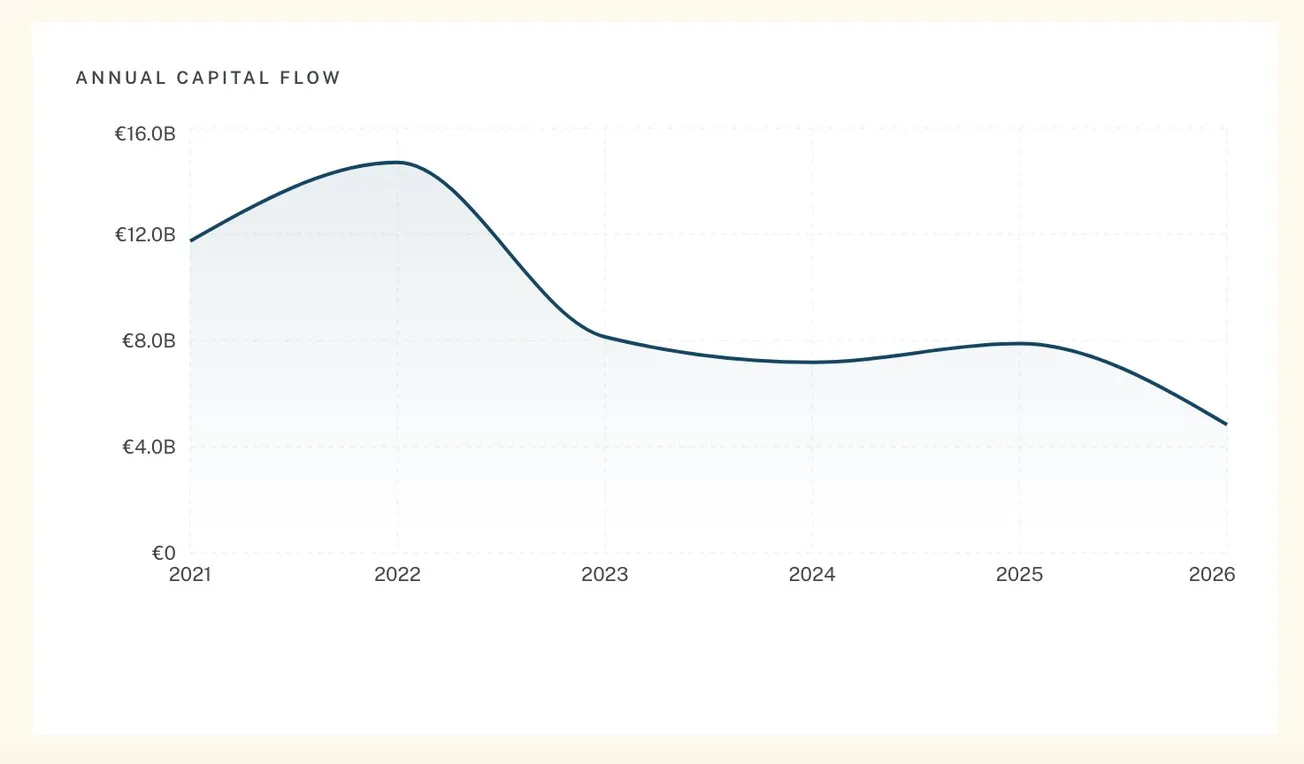

French tech raised €2.09 billion between April and June, up 16% on last year. Four companies pulled in more than €100 million each. The typical round is bigger than it's been in six years. Overall, funding in the first half of 2026 is on pace to easily surpass 2025 levels, potentially the second consecutive annual increase.

It's tempting to embrace this as confirmation that the funding rebound is real.

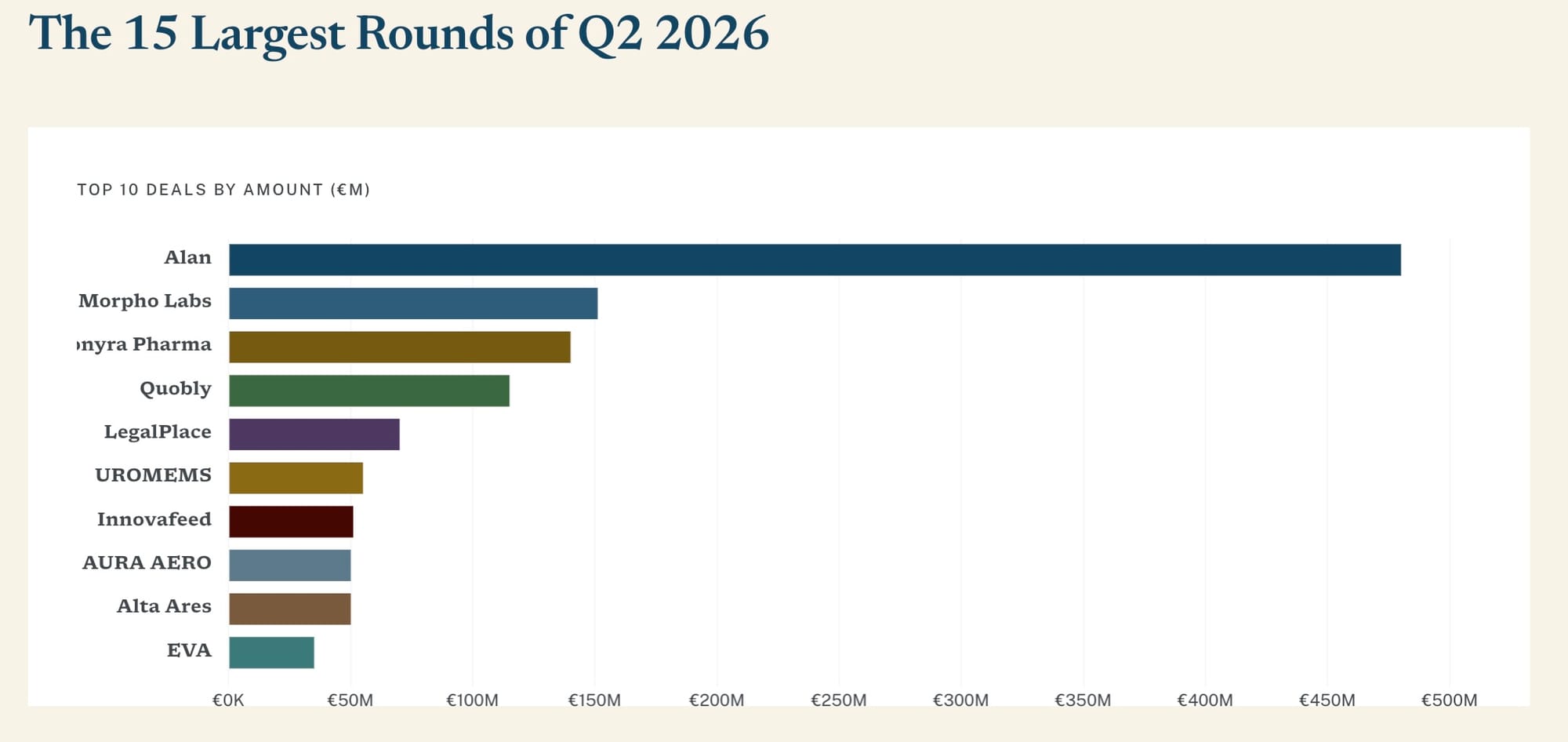

Alas, there's a catch, and it's a big one. In June, Alan, the Paris health-insurance unicorn, closed a €480 million growth round led by Index Ventures, with Prosus, Dara Holdings, and Teachers' Venture Growth alongside.

That single deal is 22.9% of everything French startups raised all quarter. Pull it out of the numbers, and the picture inverts completely. The 16% gain becomes an 11% decline.

This mirrors the €890M round by AMI Labs in Q1 2026, a huge chunk of the €2.73 billion raised that quarter. And overall, in 2025, the €1.8 billion raised by Mistral AI accounted for a big slice of the year's €7.98 billion.

In Q1, we called this the Great Concentration. This time: Top-Heavy. But in reality, it seems like the New Normal.

Which raises the obvious worry: is the market falling apart?

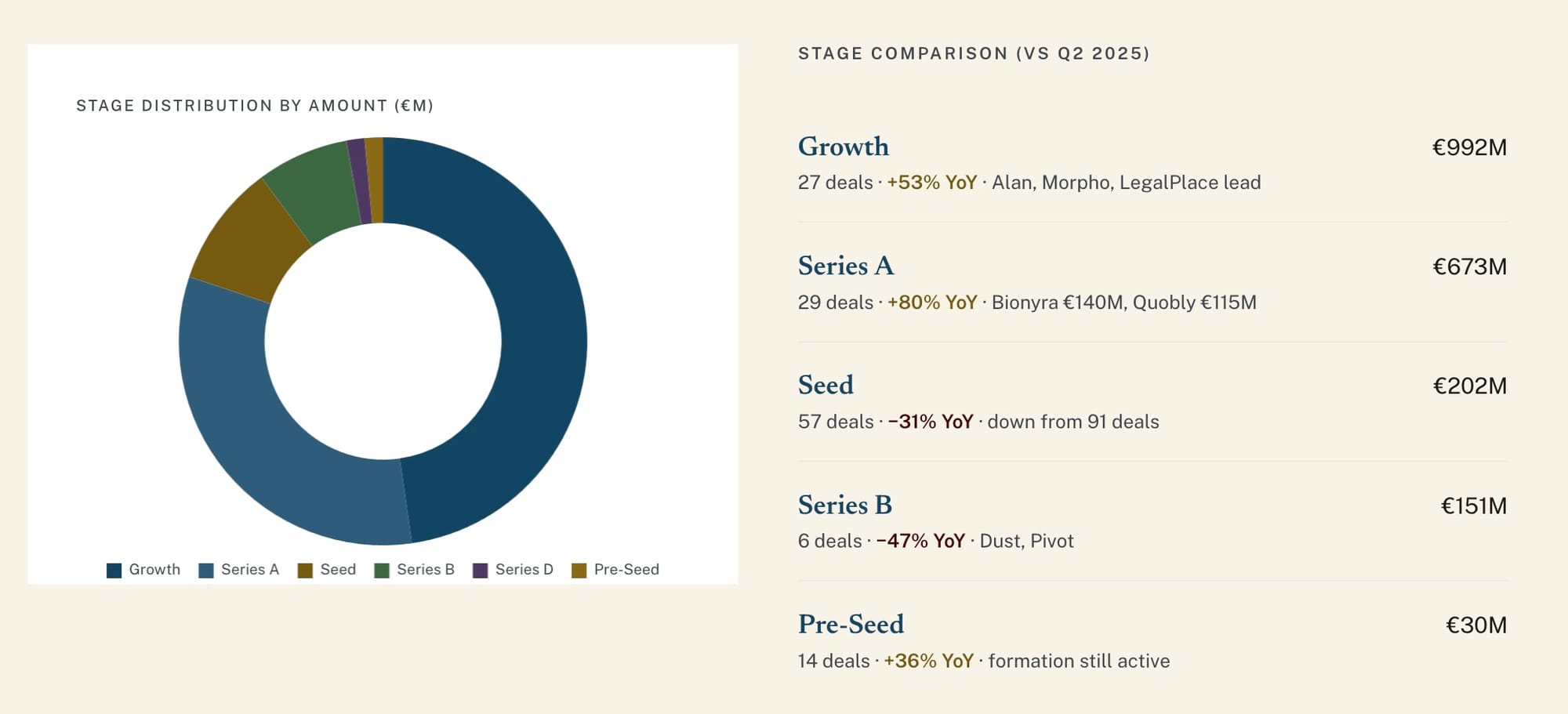

Not necessarily. The median round climbed to €5.0M, a six-year peak. Growth-stage money is abundant. Series A checks ballooned.

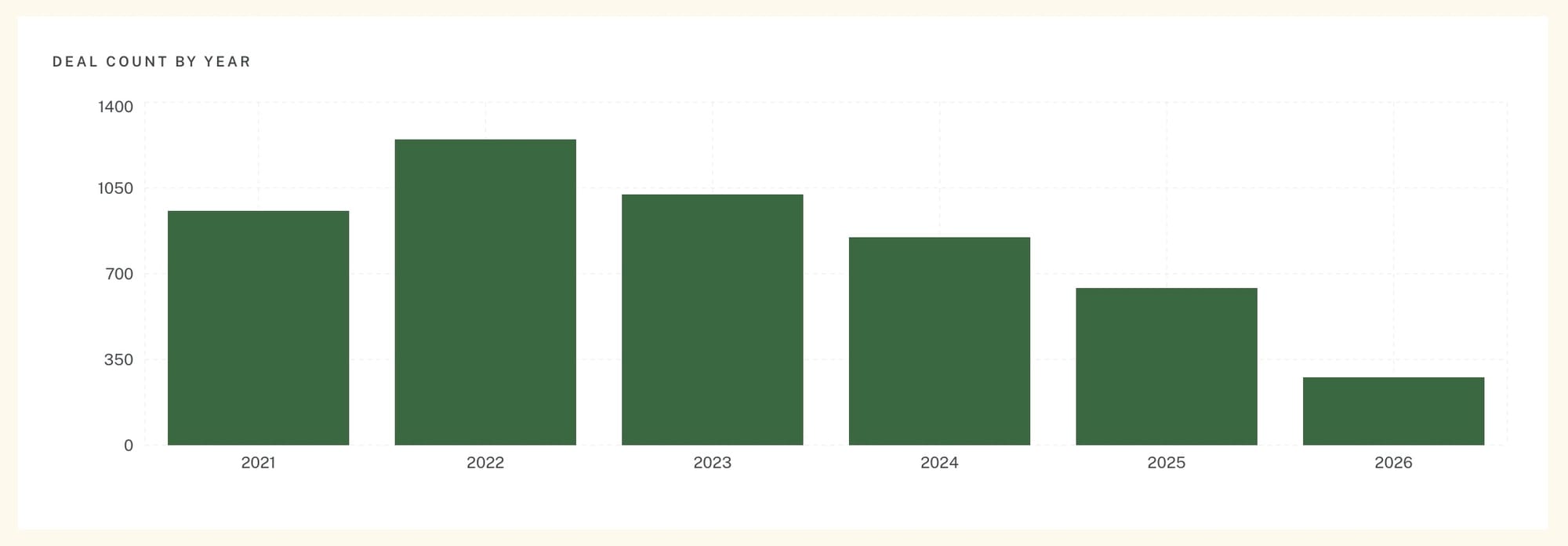

So, this isn't a market in crisis. But it is a market that has quietly stopped growing wider. Investors are doing fewer deals and shoveling more money into the ones they do. Deal count dropped 17% year-on-year, to 139. While Q1 and Q2 did exactly the same number of deals, 139 each, Q2 raised 23% less.

Again, the only real difference is the size of each quarter's headline act: Q1 had AMI Labs at €890M, Q2 had Alan at €480M. Take both mega-rounds off the table, and Q2 still trailed Q1 by roughly 12%.

Six months in, the year looks strong-ish

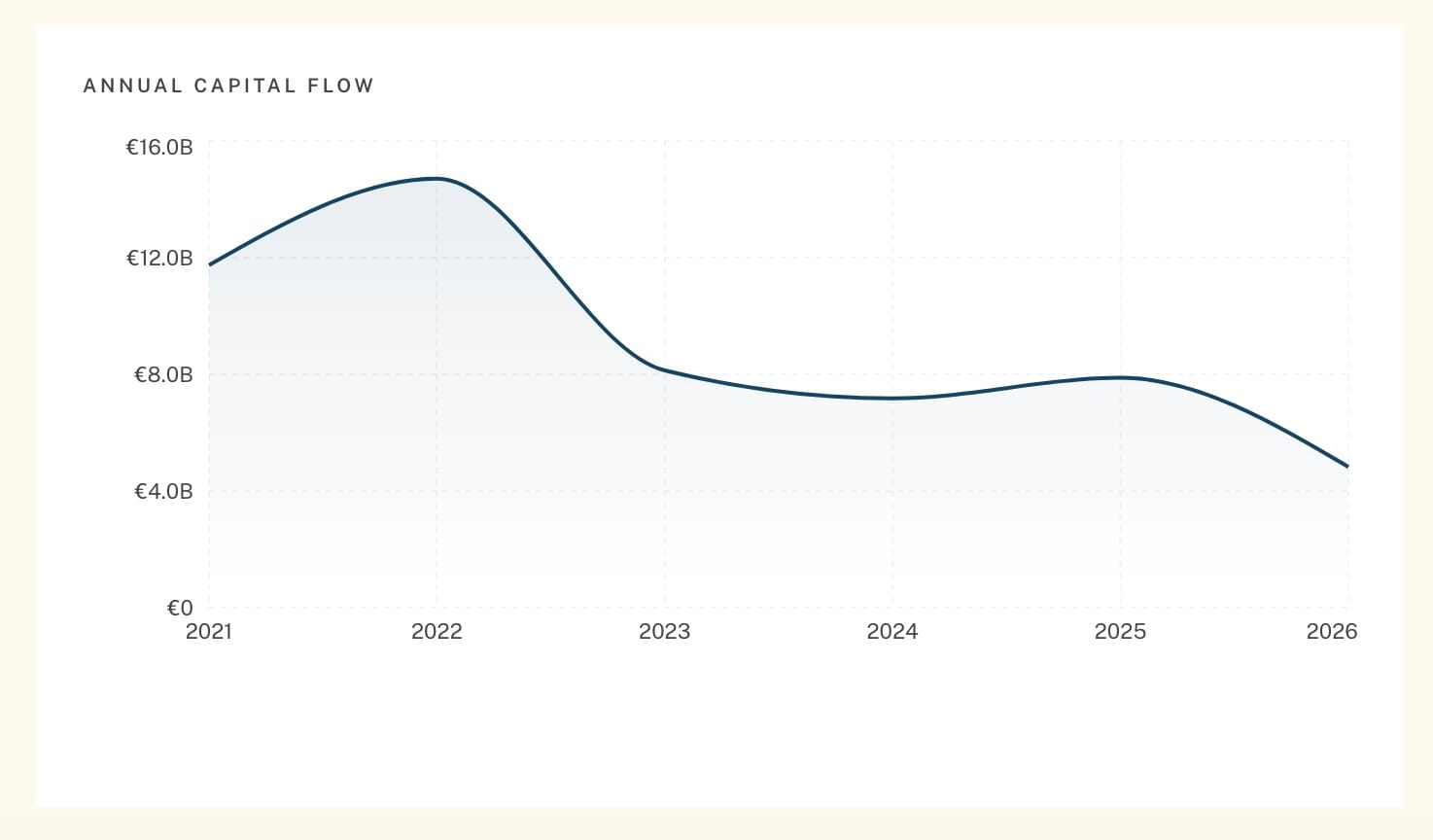

Widen out to the full first half, and 2026 starts to look genuinely good. By June, French startups had raised €4.83 billion, accounting for 61% of the total €7.98 billion for 2025. Nine rounds crossed €100M in six months, three times the H1 2025 count.

Extend the run-rate and the full year lands around €9.3–9.7B, enough to beat both 2025 and 2024 and make this France's best funding year since 2022.

Then comes the footnote, which is just the report's thesis at a higher altitude. Two rounds, AMI's €890M and Alan's €480M, add up to €1.37 billion. That's 28% of the half-year and about 91% of the entire year-on-year gain.

Remove them, and H1 2026 is roughly 4% above H1 2025, on the fewest first-half deals in six years. Flat, in other words, with two very large exceptions.

None of that stops 2026 from posting a bigger headline than 2025. It almost certainly will. It just means the market underneath the two blockbusters barely moved.

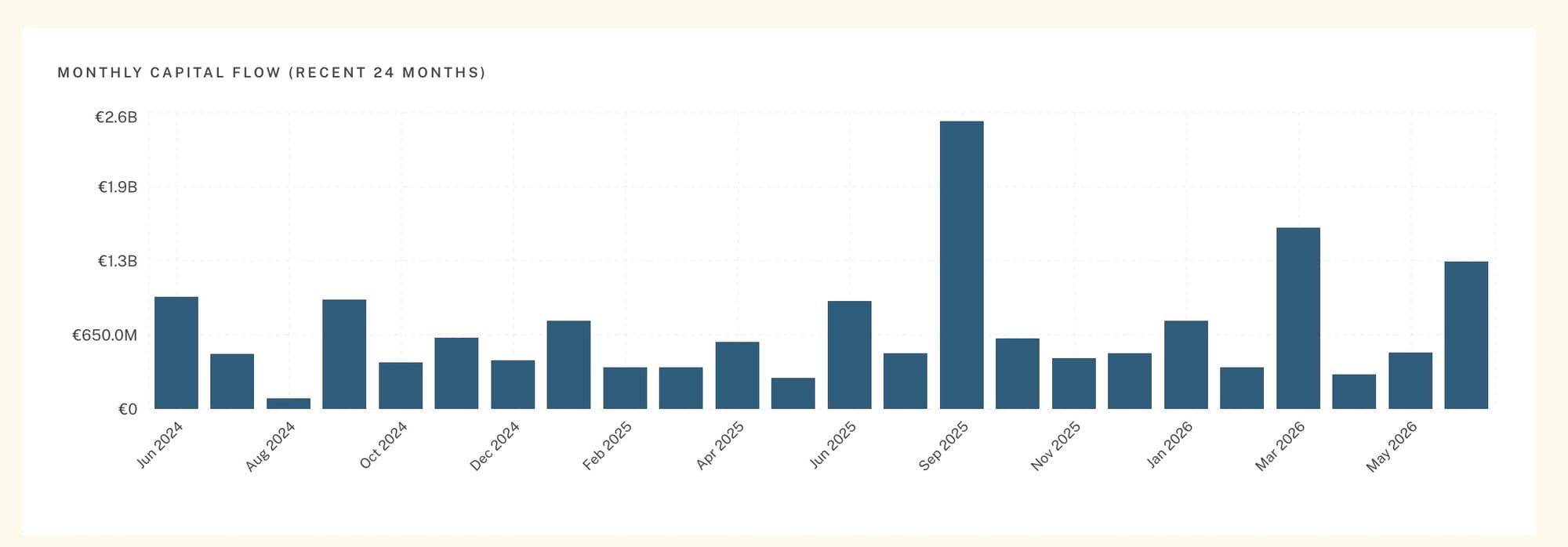

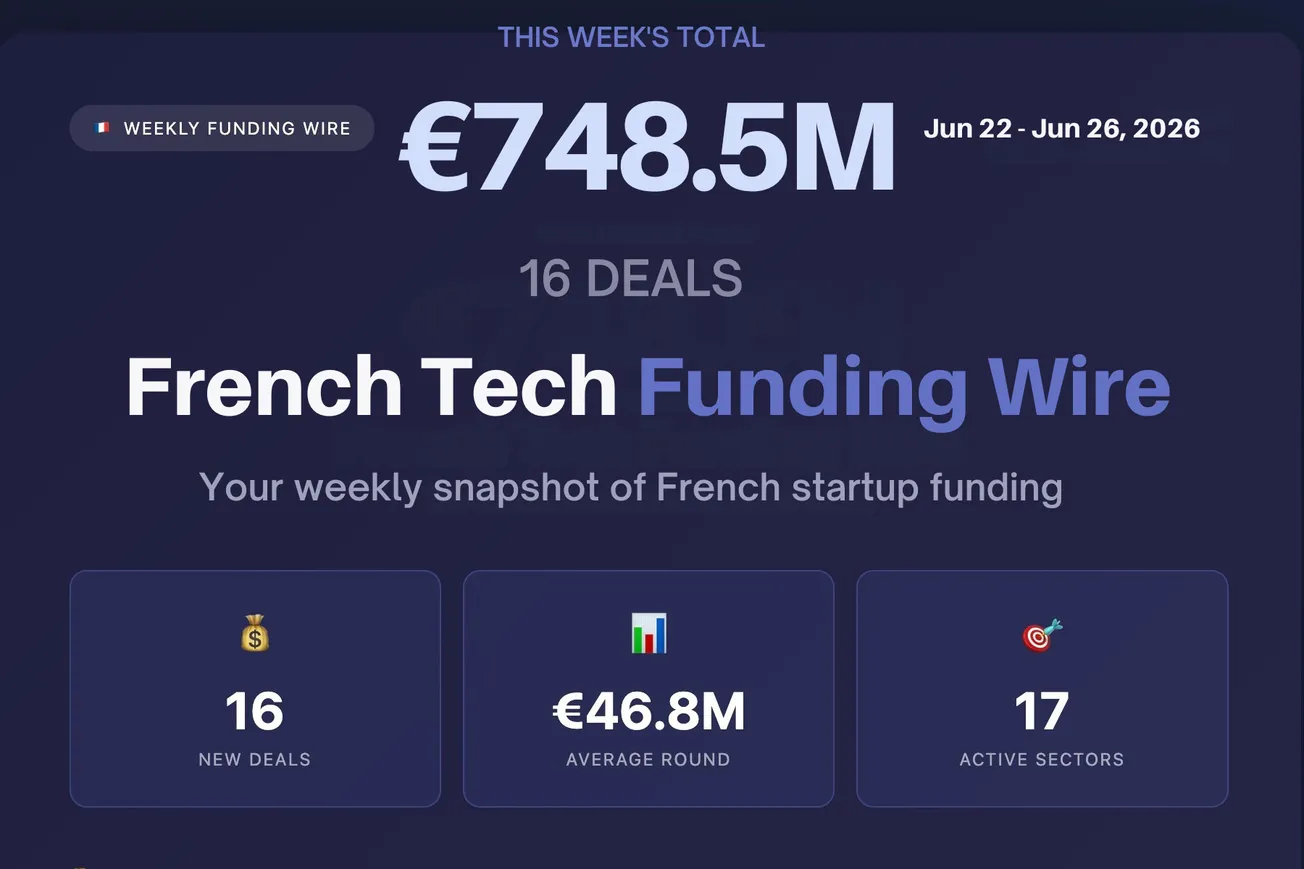

The quarter was mostly June

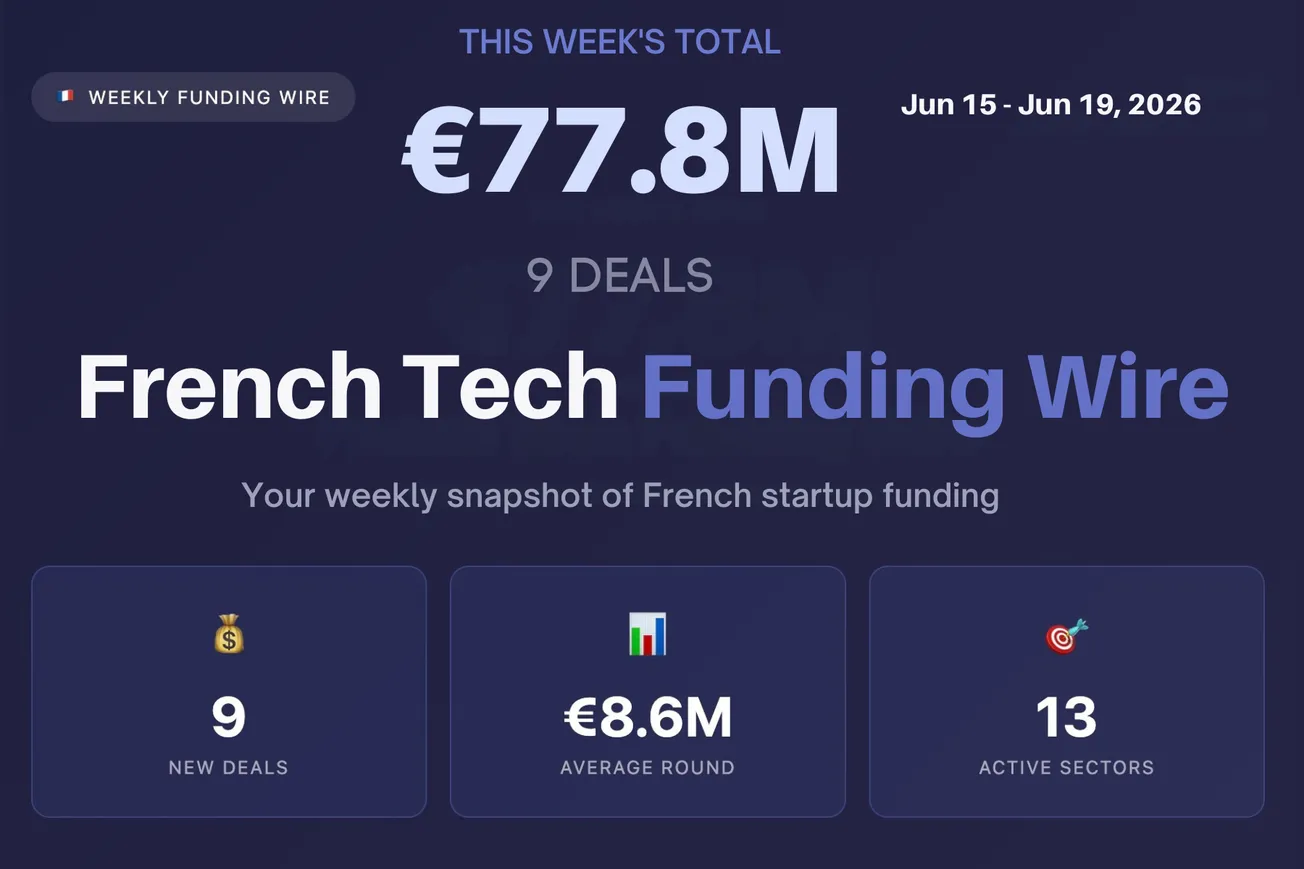

Zoom in on the three months, and the load is unevenly distributed. April was the soft spot at €305M, about half what April 2025 managed. May climbed back to €494M. Then June did nearly everything: €1.30 billion, or 62% of the quarter, with Alan, Morpho Labs (€151M) and Bionyra Pharma (€140M) all closing inside the same few weeks. Stripping Alan out, June still cleared €815M, comfortably the biggest month.

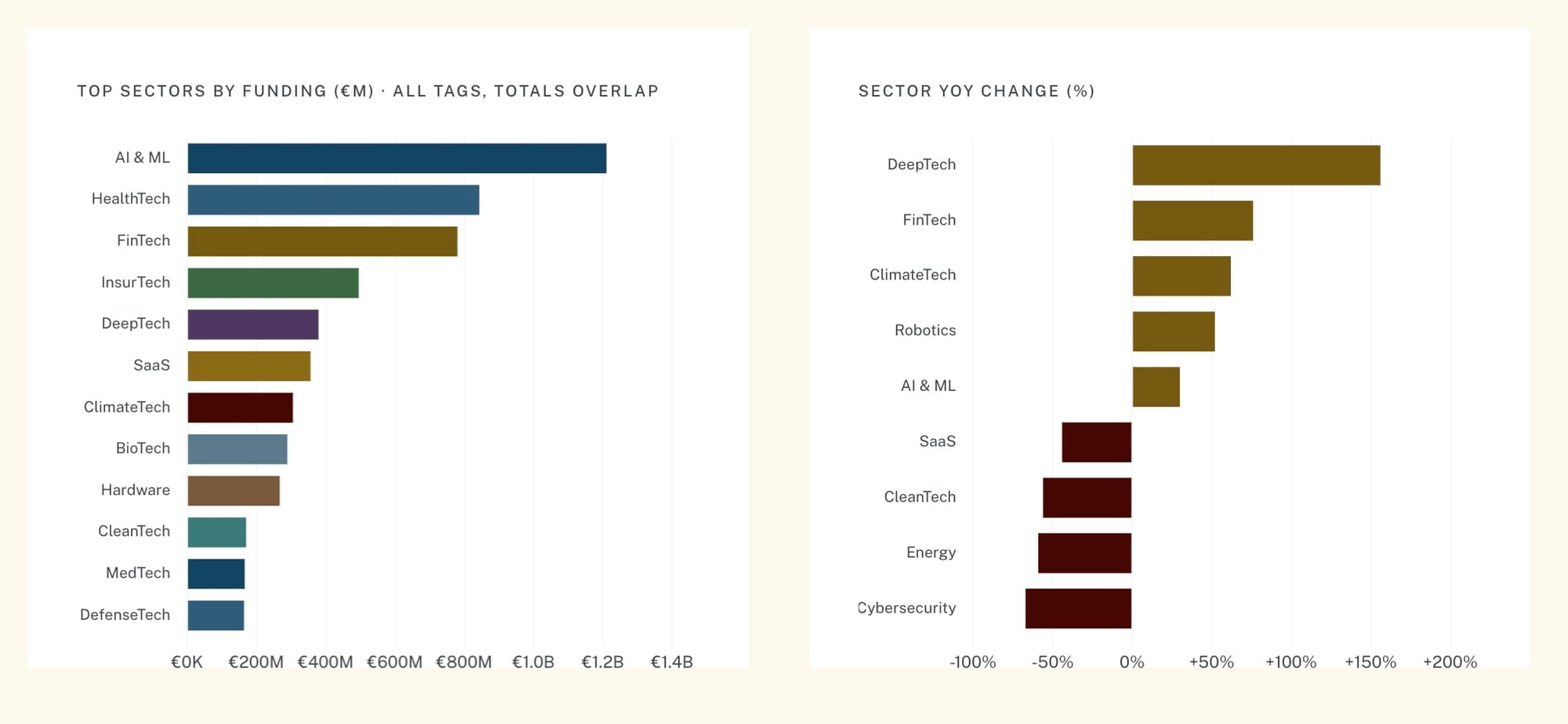

AI still eats everything

Just to restate the obvious: AI is France's dominant sector by a wide margin: €1.21 billion, about 58% of everything raised this quarter, and a six-year high, up 30% year-on-year. With the same caveat that Alan's single €480M round is tagged AI, health, fintech, and insurance, so it lifts four different sector headlines at once.

Strip out Alan and AI represents €730M, which is actually down about 21% on last year. So the underlying AI market softened even as the sector's headline hit a record.

What genuinely grew, with no giant doing the work, is deeptech and quantum: Grenoble's Quobly raised €115M, part of a €238M quarter that made Grenoble the country's No. 2 hub after Paris.

And health and biotech, ex-Alan, is up 80%, led by Bionyra's €140M Series A, one of the largest French biotech A-rounds on record. Meanwhile, SaaS (−44%), cleantech (−56%), and cybersecurity (−67%) fell.

The real story is at the bottom of the funnel

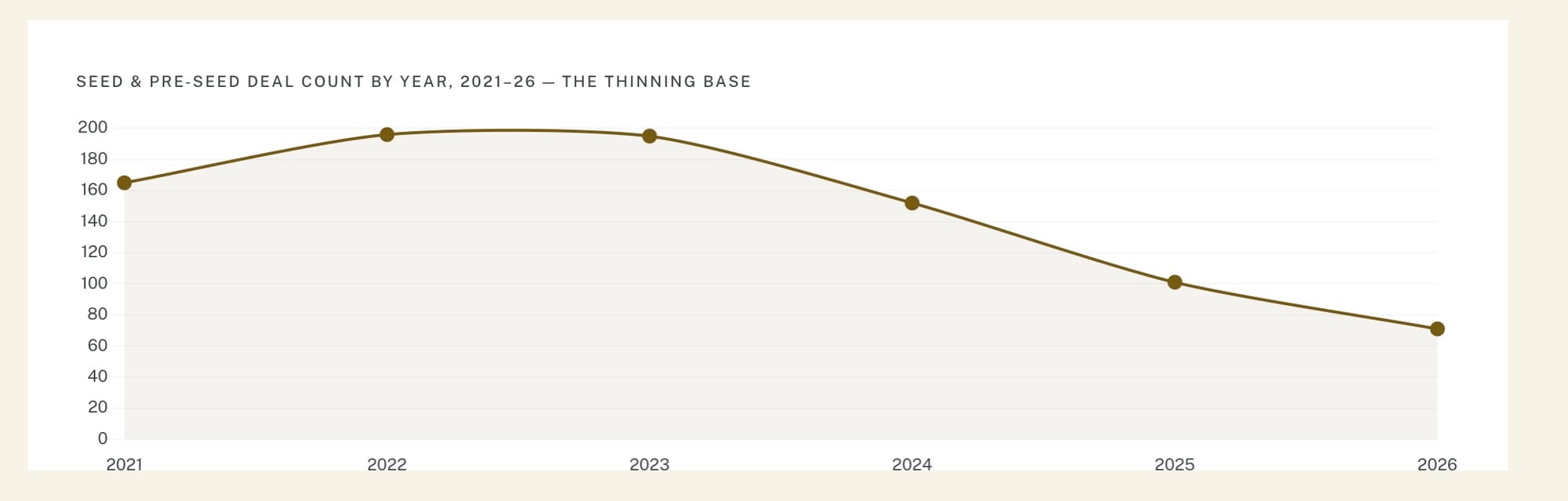

Seed and pre-seed rounds fell from 91 to 57 year-on-year. Measured against the 2022 peak of 196, early-stage dealmaking has collapsed by 64%.

Meanwhile, the top swelled. Series A did the same number of deals as last year but raised 80% more, because two of those "Series A" rounds, Bionyra and Quobly, were nine-figure cheques that would have been growth rounds in any earlier year. Growth funding itself hit €992M, near a six-year high.

The pipeline that's supposed to feed tomorrow's Series A and B is narrowing fast, while the stages it feeds are overflowing. A market can run that way for a while. It can't run that way indefinitely.

Naturally, Bpifrance continues to plug the gap. The public bank was in 22 of the quarter's 139 deals, 16% of the whole market, and more than four times the count of any private fund, and it shows up most in the exact seed rounds private capital is walking away from. The busiest private early-stage names, daphni and Kima Ventures at five deals apiece, aren't close.

More and more, the state is the floor under French seed.

Paris pulls the money back, Grenoble gatecrashes

Paris took 72% of the quarter's value, up from 59%, though most of that jump is just Alan being a Paris company (strip it, and Paris still held 64%). Regional funding dropped 20% in absolute terms.

The standout exception is worth the drive south. Grenoble raised €238M across five deals, including Quobly, UROMEMS, Mantle8, and ROSI, making it France's clear No. 2 hub for the quarter.

Three questions for the back half

How 2026 gets remembered comes down to three things:

- Does deal count finally stop sliding, or is the shrinkage permanent?

- Is Alan a fluke, or the first evidence that €300M+ growth rounds can close in France again?

- And when the full-year total lands, probably above €9 billion, how much of it will be a few giants versus a broad, healthy field?

The safe prediction is that French tech will raise more in 2026 than in 2025. The open question is whether that reflects a stronger market or just a handful of companies getting very large.

{kind=link}