One weak link can break a chain. When it comes to European tech manufacturing, the latest weak link is not metal but gas.

Just two weeks after the U.S. began its bombing campaign against Iran in late February, French industrial gas giant AirLiquide declared force majeure on helium shipments. This was followed shortly by its US subsidiary, Air Gas, on March 17th. These suppliers sourced most of their helium from Qatar, whose exports are now blocked behind the Strait of Hormuz.

This represented a severe reduction in global supply. “When the supply deficit hits, it will probably be the worst period; it will feel like a 30% deficit in supply for helium overall,” said Phil Kornbluth, the President of Kornbluth Consulting and a senior figure in the helium industry for 44 years, in a March interview with the French Tech Journal.

AirLiquide declaring force majeure meant two things, as Kornbluth described: “They will implement a supply allocation, and they will implement a significant pricing surcharge.”

Indeed, Helium spot prices are already increasing, with contract prices to follow. Helium prices in Europe have jumped 20% since March, approaching historic highs.

If you think this is mainly going to impact the cost of children’s birthday parties, think again.

High-purity helium is a fundamental element in the creation of microscopic wafers, core components of microchips and semiconductors. These tiny machines power the computers, servers, and data centers that the AI boom is built on. Helium also serves as an essential ingredient for the future of compute capabilities, cooling next-gen quantum semiconductors to frigid temperatures.

When we think of ‘critical materials’ for digital technologies, rare earths or specific metals are usually what come to mind. Yet, due to its properties, helium is irreplaceable in these roles, making it a critical material. The good news is that helium is not rare: most critical gases and key minerals for digital infrastructure are abundant worldwide. The bad news is that the existing supply chain is far from dispersed: it relies on a few key production facilities with tight margins.

The helium crisis is unfolding amid the broader debate over economic and technological sovereignty. French and European governments have become increasingly aggressive in asserting their independence in recent months, pursuing a series of policies and purchasing decisions aimed at reducing their reliance on international partners and corporations.

For all the attempts to strike an independent posture, the helium crisis is a reminder of just how deeply intertwined economies and supply chains have become after decades of globalization and free trade agreements.

For digital technology companies in France and abroad, helium is in critical short supply, a shortage for which key players such as the industry association France Chimie and the national research body CNRS are already sounding the alarm. The crisis could seriously endanger projects for digital technology sovereignty and underscores vulnerabilities in Europe’s current approach to critical materials.

What's at stake for French tech?

On the front lines of the helium shock, French technology laboratories, the long-touted advantage for French tech in the digital and AI fields, are being hit hard. The Centre National de Recherche Scientifique (CNRS) had already raised alarms in 2025 on the increasing difficulty of acquiring helium for R&D, with the cost per liter exploding from €5 in 2018 to €35 in 2023, representing a yearly cost of around €2 million for the CNRS in 2025.

CNRS had already gone through one shock when Russia’s invasion of Ukraine in 2022 led to sanctions against Russia, one of the few nations that exports helium. Another 20% increase will hurt laboratories, yet this percentage might grow even further. In Asia, Fitch Ratings has predicted that spot helium prices could jump between 50% and 200% in severe scenarios, and contract prices could decline by 20% to 40% upon renegotiation. What happens in Asian markets will have echoes in Europe.

European semiconductor manufacturing, a cornerstone of Europe’s technological sovereignty, is also at risk of shortages or price increases due to this irreplaceable gas. Demand from the semiconductor processing sector was already outpacing supply, and is expected to account for 20.9% of the helium market by 2035, so this new crisis comes at a bad time. A reduced helium supply means less chip production, and more expensive helium will put pressure on profit margins.

According to European governments, not all is lost. The French government is insisting that Europe will not face shortages, though it will face higher prices.

In a recent French Senate hearing, the Minister of Economy Roland Lescure underlined that in terms of resources, “France is faced with a price shock, not a volume shock.” Regarding helium and petrochemicals, he later briefly added: “There is no major short-term risk identified for industrial sectors.”

Europe’s little fish meet global markets and allocations

While governments hold out hope, the reality is that Europe faces a distinct disadvantage in many critical materials, which the helium crisis is already underlining.

Somewhat surprisingly, the disadvantage is not related to a lack of regional production or geopolitical power. Instead, it comes from market logic.

These markets are global, not regional or national. Helium is only produced by a few countries: Algeria, the United States, Russia, and Qatar. And then it is distributed by a few major companies worldwide. While AirLiquide may be headquartered in France, as Kornbluth said, “these are global suppliers; they usually manage the shortage globally.”

So when helium shocks hit, who gets hurt the most is determined by allocations, which is detrimental to small players in the global economy.

Upon declaring force majeure, a supplier must establish allocations and is allowed to “prioritize applications that are viewed as more critical.” Kornbluth pointed out that “MRIs, semiconductors, aerospace and nuclear power generation” are at the front of the line and “are going to get relatively higher allocations.”

Allocations are bad news for European advanced electronics laboratories, which have a lower priority. Labs in the US have already faced severe cuts, and European tech may face the same challenge. In the case of French labs, a price shock could easily lead to a supply shortage, slowing the development of European wafers and chip technologies at a critical moment.

European semiconductor manufacturers seem more secure in their priority sector. However, the problem deepens with the second main consideration for allocations: contract size.

Suppliers will prioritize the largest and most reliable contracts, as Kornbluth highlights, and while semiconductor manufacturers usually have the means to pay higher prices, not all companies are made equal. European companies generally have smaller war chests than their larger foreign competitors.

Financially speaking, European manufacturers are little fish in a big pond, which can pose a serious risk when allocations are made. Compared to larger firms in Asia and North America, helium contracts with European plants, STMicroelectronics in Crolles, and the FAMES pilot line in Grenoble may not be prioritized for full allocations. Adding fuel to the fire, these smaller firms are also less able to absorb supply and price shocks than their larger competitors.

The French Plan: a model for critical resources?

Given its market disadvantages and geopolitical woes, what solutions can Europe adopt to secure critical materials and mitigate the impact of price shocks? A recent French proposal may provide the needed framework.

On May 5th, 2026, Minister Lescure delivered a speech in the Lacq basin, where he unveiled the new ”national strategic plan for rare earths and permanent magnets”. Going through his statement and the government-published plan's measures, one need not read between the lines to see that the objective is for France and Europe to have the option of self-sufficiency if the need arises. The plan aims to cover 10% of global demand for heavy rare earths, which it defines as 100% of European demand. Similar ambitions are set at 25% of European light rare earths and 50% of permanent magnets.

The levers to achieve this goal are familiar: supporting reindustrialization and investing in new projects. The government has laid out three pillars to gain more control over its critical mineral supplies: national-interest projects, strategic guarantees, and bilateral agreements.

France aims to designate more rare-earth and permanent-magnet projects as ‘of national interest,’ thereby allowing firms to expedite their permitting and construction. Next, the state wants to provide purchasing guarantees to these firms to give them some long-term stability and protect them against market shocks and larger competitors.

Finally, France is not just building these projects on its own territory. The plan envisages a web of bilateral agreements coming together to form a dispersed supply chain with more friendly partners, without being dependent on any one country. France has signed over 20 bilateral agreements to this end: rare earth extraction agreements with Sweden and Brazil; magnet materials agreements with Australia; terbium and dysprosium agreements with Mongolia; scandium and lithium agreements with Canada; and refining agreements with Namibia. Many agreements aim to make France into a refining hub. For instance, rare earths extracted in Sweden will be refined in La Rochelle, and Japan has agreed to fund the construction of another refinery in Lacq.

This comes together to form one system, a web of friendly countries, with multiple small suppliers for every resource, supported by bilateral agreements and state guarantees for smaller firms.

This system still poses a difficult-to-avoid risk. Dispersion means more potential failure points. A change of government in Brazil or Kazakhstan would not cut off the whole supply of any given rare earth, but could reduce supply by a significant percentage. Disruptions to global trade routes could still block off supplies from distant countries like Australia and Mongolia. Yet this risk still represents a significant improvement from the current supply chain, with its major fragilities and dependencies.

The French plan holds water when it comes to building up supply. However, it might not reassure European technology labs and tech manufacturers.

This increased French production could still be sold and allocated to the highest bidders, who would likely be outside Europe, if a major shock occurred in the rare earths or permanent magnets markets.

The same market logic driving today’s crisis will persist tomorrow, and while French rare earth refiners may have state guarantees, no such guarantees exist for French technology companies, which will desperately need those resources.

A possible solution rests in another tool: reserves. This alternative, state-held source can act as a critical vessel to stabilize supply and prices.

The EU has already laid the groundwork for identifying and prioritizing key materials with the Critical Raw Materials Act. France, Italy, and Germany are engaged in a new initiative to build up reserves of Europe’s 34 critical raw materials, which include rare earth metals and permanent magnets, and was recently updated to cover helium as well.

It is possible, though, that helium and other ‘less essential’ resources will receive less attention and priority. The recent French plan, for example, does not cover helium. Risks for the technology sector may also arise from resources that the EU does not currently label ‘critical’, such as neon.

Whether these efforts yield results, specifically strategic reserves and concrete infrastructure, will have a significant impact on the stability of the European technology industry moving forward.

History shows that building reserves of key gases can be feasible and effective. This was once the case for helium in the US: the Federal Helium Reserve in Texas used underground storage to provide a key lever in times of supply turbulence. However, the US federal government decided to sell its reserve starting in the 90s and sold off the site in 2024.

Helium was also removed from the US critical minerals list on two occasions and was not included in the 2026 Project Vault because it is not sufficiently vulnerable to domestic disruptions or supply-point failures.

The Peterson Institute for International Economics criticized this decision, pointing out helium’s critical nature, concentrated production, and the need for specialized storage infrastructure at scale.

They highlighted that the cost of maintaining a helium reserve is modest compared with the 1 billion USD spent annually on semiconductor production.

However, even reserve storage may not be sufficient to protect the little fish of European tech from global currents. In the current oil and gas shock, countries like the United States are facing similar increases in fuel and gasoline prices, despite the US government holding large oil reserves and producing oil in large quantities. Consumers and laboratories in the US are suffering from allocations and shortages.

For global commodities, price shocks impact across regions and borders. European strategic reserves of critical materials may still be sold off to the highest bidder, who will likely not be European consumers, European tech labs, or European manufacturers.

If Europe wants to go beyond easing global price shocks and shore up its domestic industries, Brussels and member states may need to see how they can guarantee industrial supply in times of crisis.

A new helium hope?

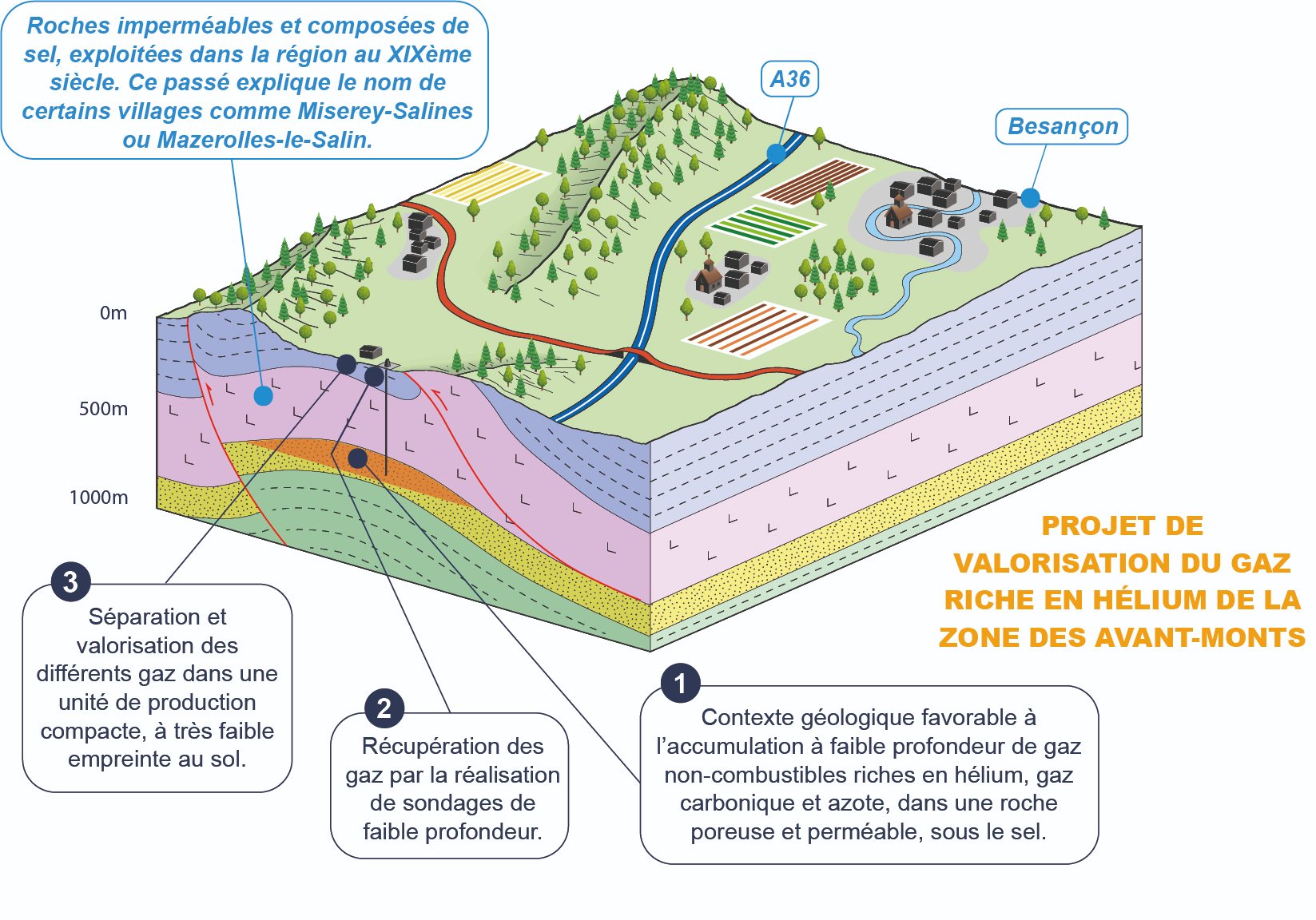

While it remains a long shot, perhaps, a company called 45-8 Energy believes the real solution to France’s helium problem is within reach. Founded in Metz in 2017, 45-8 ENERGY specializes in the exploration of naturally occurring helium and hydrogen, two gases that are increasingly viewed as strategic resources for Europe’s energy and industrial future.

The company has spent years combing through historical geological records, identifying promising sites where helium-rich gases naturally seep to the surface. What began as a niche exploration effort has evolved into one of Europe’s most advanced attempts to build a domestic helium industry.

Much of 45-8 ENERGY’s work has focused on two key exploration areas in eastern and central France, including projects in the Doubs and Nièvre regions. The company has carried out extensive geological surveys, airborne geophysics campaigns, seismic studies, and exploratory drilling to better understand the underground systems that trap helium.

In 2022, it achieved a European first by extracting helium from a pilot site in the Nièvre department, demonstrating that commercial production could be feasible on the continent. Along the way, the company has worked closely with scientific partners such as BRGM, CNRS, and regional universities, while also contributing to broader research efforts to map France’s untapped helium potential.

Its timing couldn’t have been better. In the wake of the Russian invasion of Ukraine and the previous helium crisis, 45-8 ENERGY secured €2.88 million in funding through the France 2030 investment program to accelerate development of its helium project in Doubs, a recognition of helium’s status as a critical raw material for sectors ranging from medical imaging and semiconductors to aerospace.

The company has since been in the exploration and pilot production phase, but it has continued to secure multiple exploration permits and work toward industrial-scale production. Then, last month, the company made a breakthrough announcement: a deep drilling campaign at its Fonts-Bouillants license in the Nièvre region had identified helium- and nitrogen-rich formations at depths of up to 1,500 meters.

According to the company, the most promising zones sit between roughly 900 and 1,250 meters underground and could produce more than 70,000 cubic meters of gas per day, with helium concentrations ranging from 0.31% to 0.35%. Those concentrations are significant because helium is typically produced as a byproduct of other gases, and the economics depend heavily on both concentration levels and flow rates.

This discovery pushes the project beyond geological curiosity and closer to a commercially viable source of domestically produced helium. The company doesn’t expect to find a hidden massive reserve.

Instead, the latest finding bolsters its belief that a network of such pockets exists. If the company can meet its target of supplying at least 15% of France’s helium, the country would have a cushion to ensure supply for its most urgent needs in a time of crisis.

"It's not a gigantic deposit. It won't make France self-sufficient," a company official told local media. "But we are very pleased with this discovery, which will allow us to ensure strategic uses."

{kind=link}